The finances of some 60,000 consumer and 11,000 business accounts across 32 Republic Bank locations in three states are now managed by the 142-year-old, Lancaster, PA-based bank.

By Matt Skoufalos | April 29, 2024

Fulton Bank acquires Republic Bank in FDIC transaction. Credit: Matt Skoufalos.

On Friday, the Pennsylvania Department of Banking and Securities closed the Philadelphia, Pennsylvania-based Republic Bank, N.A., “citing unsafe and unsound condition, in order to protect depositors,” according to a public statement.

The Department named the Federal Deposit Insurance Corporation (FDIC) as receiver of the bank and its assets, and the federal regulatory agency subsequently signed an agreement with Lancaster, Pennsylvania-based Fulton Bank, N.A. “to assume substantially all of the deposits and purchase substantially all of the assets of Republic Bank,” according to FDIC.

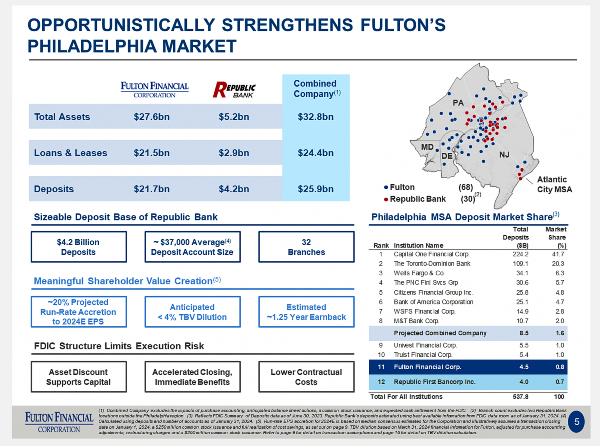

The agreement is a purchase and assumption transaction, in which Fulton Bank purchased some $6 billion in Republic Bank assets, including some $2 billion in investments and nearly $3 billion in loans.

Fulton also takes on approximately $5.3 billion in assumed liabilities from Republic, including $4 billion in deposits and about $1.3 billion in other liabilities.

The deal creates a combined company, Fulton Financial Corporation, with total assets of $32.8 billion, loans of $24.4 billion, and deposits of $25.9 billion.

Fulton projects that the end result will position the combined entity into the ninth-largest banking entity in the Philadelphia metro area by total deposit, behind M&T and above Univest.

On a call with investors Monday morning, Fulton Bank Chairman and CEO Curtis Myers described the acquisition as “an immediate and strategic opportunity to grow and serve the communities that we already know.”

Adding 60,000 consumer customers and 11,000 business customers from Republic Bank “nearly doubles our presence” in the region, he said.

For the remainder of the year, Fulton Bank will work to get the absorbed operations of Republic Bank down to a standalone run rate of some 40 percent less than its current, annualized $100-115 million, Myers said.

However, the CEO added that doing so doesn’t necessarily mean cutting jobs or closing branches — at least not right away.

Combined Fulton and Republic Bank position. Credit: Fulton Bank investor call.

Due to the FDIC facilitation of its acquisition of Republic Bank assets, Fulton Bank has 60 days to decide the fate of those leased facilities, and 90 days to decide on its owned properties.

“Building out the franchise is a big strategic value here,” Myers said. “The benefit of an (FDIC) assisted transaction is we get the financial centers operating and a period of time to analyze it to decide.”

Republic Bank employees will be paid for at least the next 90 days as well, he said. Fulton Bank views the added workforce as a strength, and not a drawback, to the deal.

“We really feel that the Republic team has done a great job creating customers and holding onto customers,” Myers said. “We think we can navigate this in a way that we don’t have attrition risk.

“We’re doubling the size in our core metro market,” he continued. “This is a growth opportunity for us; we’re not focused on short-term costs.”

For customers, Fulton Bank spokesperson Lacey Dean said the transition “should be seamless,” with Republic Bank cards, accounts, checks, and branches all operating as they did prior to the changeover. Any additional changes will be communicated in the coming weeks and months.

“There’s really nothing that they need to do at this point,” Dean said. “We are really excited to welcome these folks to Fulton Bank.”

(FDIC published a customer FAQ for the transaction, which is viewable here.)

Established on September 6, 1988 as Republic Bank, the financial institution became Republic First in 2001, and then reverted to Republic Bank in 2010.

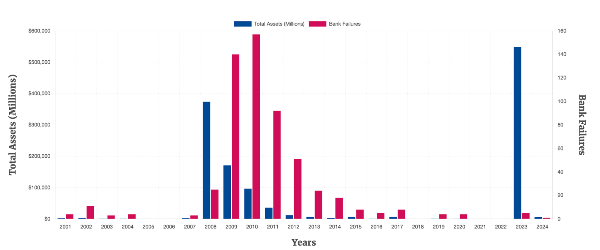

FDIC recent history of bank failures in America. Credit: FDIC.

Across its lifespan, Republic grew to operate 32 locations across New Jersey, Pennsylvania, and New York, with 18 branches in South Jersey, including seven in Camden County (Berlin, Haddonfield, Gloucester Township, Sicklerville, Voorhees, and two locations in Cherry Hill).

Despite its broad local reach, Republic Bank seemed to be chasing customer deposits to underwrite spiraling lending costs. Tyler Roush of Forbes chronicled a number of benchmarks in its decline, including hits to its mortgage loan portfolio, uninsured customer deposits, and a postponed shareholder meeting.

“In 2022, Republic First’s financial auditor (Crowe LLP) told the bank it had “material weaknesses in internal control over financial reporting,” according to a regulatory filing,” Roush wrote. “That auditor was dismissed by Republic First in February.”

In a brief review of its uniform bank performance report (UBPR), Dante Tosetti, an expert in regulatory compliance for financial institutions, noted that interest expenses at Republic had more than quadrupled, climbing from 0.53 percent at the end of 2022 to 2.44 percent at the end of 2023.

“That impacted their earnings, and brought them into the red,” Tosetti said. “The interest-rate environment went up, and they had to attract deposits to continue to fund their loans.”

At year’s end 2022, Republic had reported a net income of $11.49 million against average total assets of $5.96 billion. By year’s end 2023, the bank reported a $42-million loss against average total assets of $6.342 billion.

Those same interest-rate increases may have affected its longer-term securities holdings, driving down their value, and making it harder to unload them without taking a loss, Tosetti said.

In the broader landscape of bank failures, the peak of which stretches back to the crises of 2008 through 2014, shuttering one bank with $6 billion in assets is a blip on the radar. The failure of Republic Bank pales in comparison to even the 2023 closures of five banks that commanded more than half-a-trillion dollars.

Nonetheless, Tosetti said that “many, many banks are in the same position with balance sheets that are catawampus.

“You go back to the last crisis, everybody thought home values were going nowhere but up,” he said. “This crisis was caused by the thinking that interest rates were never going to go up.

“We’re not out of the woods yet, from a macro perspective.”